Bankruptcy

A bankruptcy is a legal proceeding under Canada’s Bankruptcy and Insolvency Act in which you must surrender certain assets and make payments based on household size and proportion of the household income to settle your debts.

Mike Wright & Associates will file documents with the Office of the Superintendent of Bankruptcy, and you will be formally declared bankrupt. From that point on, Mike Wright & Associates will deal directly with your creditors on your behalf.

Once you have been declared bankrupt:

- you will stop making payments directly to your unsecured creditors, which include credit cards, lines of credit, personal loans, payday loans and income tax debt. In fact, you won’t ever have to pay those debts if you declare bankruptcy;

- any garnishments against your salary will stop;

- any lawsuits against you by your creditors will also be stopped.

You will not lose everything when you file for bankruptcy, as some of your possessions will be protected by provincial exemptions. You may have to give up certain assets in order for Mike Wright & Associates to pay your creditors a portion of the money owed to them. In B.C., for example, clothing, household furnishings and appliances worth up to $4,000, a vehicle worth up to $5,000 and work tools worth up to $10,000 are some of the items that are exempt. Home equity of $9,000 is exempt in all areas of B.C. except in Victoria and Vancouver, where the number is $12,000.

Secured debts are not protected by a bankruptcy filing, which means debts like a mortgage or car loan must continue to be paid. If you do not make those payments, your creditors can repossess your home or your vehicle.

Once you have declared bankruptcy, Mike Wright & Associates will notify your creditors, who may hold a meeting to obtain information, appoint inspectors or give instructions. You will be required to attend that meeting if it is called, and you might even have to be examined under oath by the Office of the Superintendent of Bankruptcy about your conduct, the causes of the bankruptcy and the state of your property. You will also have to attend two counselling sessions.

When you file for bankruptcy, you must do the following:

- disclose information about all of your assets and liabilities;

- advise of any property that was sold, transferred or disposed of in the past few years;

- surrender all your credit cards;

- advise in writing of any address changes.

Once you have been declared bankrupt, Mike Wright & Associates will sell your assets, including any acquired during your bankruptcy. Assets that are exempted by provincial and federal laws are excluded from this sale. Mike Wright & Associates will hold the money raised by the sale in trust for distribution to your creditors.

You might also have to make surplus income payments during the course of your bankruptcy. Surplus income is the part of your earnings that exceeds the amount of income a family needs to maintain a reasonable standard of living, and it is set by the Office of the Superintendent of Bankruptcy annually. The larger your family, the more you are allowed to keep; the more you earn, the more you are required to contribute. If your surplus income is more than $200 per month, you will be required to contribute 50% of that amount.

If it is your first bankruptcy and you are not required to make any surplus income payments, you will be discharged from your legal obligation after nine months. You will still be required to make alimony and child support payments, student loans (if you stopped being a student less than seven years ago), court-ordered fines or penalties and debts arising from fraud. If you are required to make surplus income payments, your bankruptcy will be extended to 21 months and you will be required to make payments from your surplus income.

If it is your second bankruptcy and you are not required to make any surplus income payments, you will be discharged from your legal obligation after 24 months. If you are required to make surplus income payments, your bankruptcy will be extended to 36 months.

A person who declares bankruptcy is assigned the lowest possible credit score, which is removed after a certain period of time. Generally, it will be removed after six or seven years for a first bankruptcy and after 14 years for subsequent bankruptcies.

Division One Proposal

Blah blah blah some text

Division Two Proposal

Blah blah blah some text

What's Protected

- Most retirement savings are protected.

- Some life insurance has a cash value. Some life insurance is term life that only pays when you die. If the beneficiary of the plan is the spouse, child, parent or grandparent of the policy owner, then it is protected

- RRSPs are typically safe as well. Some of them are governed by insurance rules, where the beneficiary of the plan is the spouse, child, parent or grandparent of the policy owner, then it is protected

- all RRSPs have protection for money that’s been in the plan for more than a year

- RDSPs (Registered disability savings plans) are fully protected

What's Not

- RESPs have no protection (we generally do a payment plan to repurchase the value. it may say there’s $10,000 in there, but if it gets cashed out the government takes back the money it has contributed through learning bonds and grants; the interest is lost.)

- Tax-free savings accounts are not protected

- Most recreational assets—dirt bikes, campers, trailers, quads, jet skis, boats — are not protected

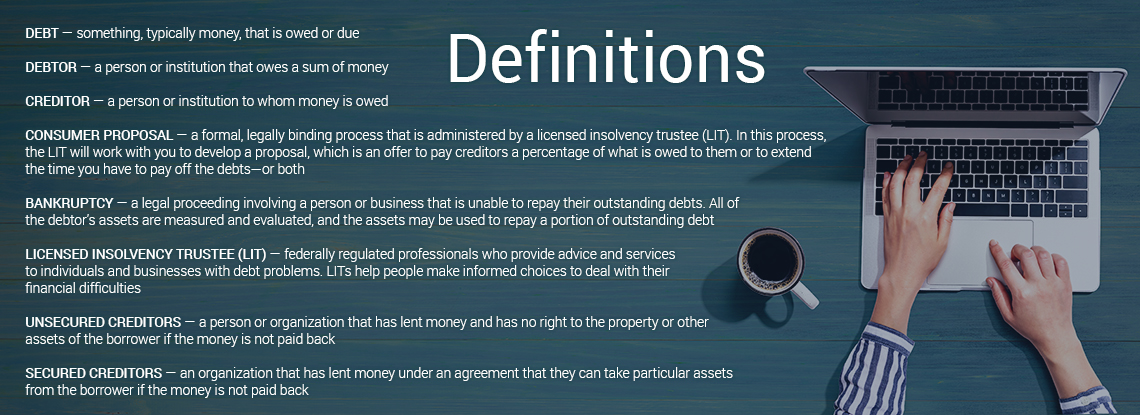

Definitions