Consumer Proposal

A consumer proposal is a legal proceeding under Canada’s Bankruptcy and Insolvency Act that allows someone to get out of costly interest rates, pay back a percentage of what they owe and get a fresh start. A proposal is recommended if you have consumer debt greater than $5,000 but less than $250,000 (excluding your mortgage) and want to stop all interest charges, wage garnishments and threats of legal action.

Mike Wright & Associates will work out an agreement with creditors on your behalf to pay a percentage of what is owed to them or to extend the time you have to pay off your debts—or both. The percentage paid, which is interest-free, will be divided among your creditors, and you will make payments to Mike Wright & Associates. The amount will depend on your income, on the value of your assets and on the creditors, because they all have different expectations.

Once an agreement is in place, you will make monthly payments for no more than five years, and there are no additional fees or service charges that other lenders might add to your bill. The process allows you to avoid bankruptcy, protect assets like your home and vehicles, and make manageable payments. The negotiated settlement comes from the income you make every month after you have paid household bills.

What happens when you file a consumer proposal:

- Mike Wright & Associates will file the proposal with the Office of the Superintendent of Bankruptcy. Once your proposal is filed, you stop making payments directly to your unsecured creditors. In addition, if your creditors are collecting your salary through garnishment of wages or have filed lawsuits against you, these actions are stopped.

- Mike Wright & Associates will submit the proposal to your creditors. The proposal will include a report on your personal situation and the causes of your financial difficulties.

- Creditors have 45 days to either accept or reject the proposal. They can also do this either prior to or at the meeting of creditors, if one is held.

There is always a chance your proposal will be rejected, but that does not mean the end of the process. Mike Wright & Associates will work with you to adjust the proposal to make it more attractive to your creditors, or perhaps they will look at other options.

You are required to give Mike Wright & Associates a complete list of your assets and liabilities, and you must advise them in writing every time your address changes.

A meeting of creditors is held if one is requested by one or more creditors, provided they are owed at least 25% of the total value of the proven claims. The number of votes corresponds to the total dollar value of the proven claims, and the vote is decided by a simple majority of this dollar value.

Another type of consumer proposal is a Division I proposal, but it is filed only if you have more than $250,000 in debt. Unlike a consumer proposal, a rejected Division I proposal means you automatically become bankrupt.

One thing to keep in mind about a consumer proposal is if you miss three monthly payments or if your payment schedule is less frequent but your last payment is more than three months past due, the proposal will be deemed annulled.

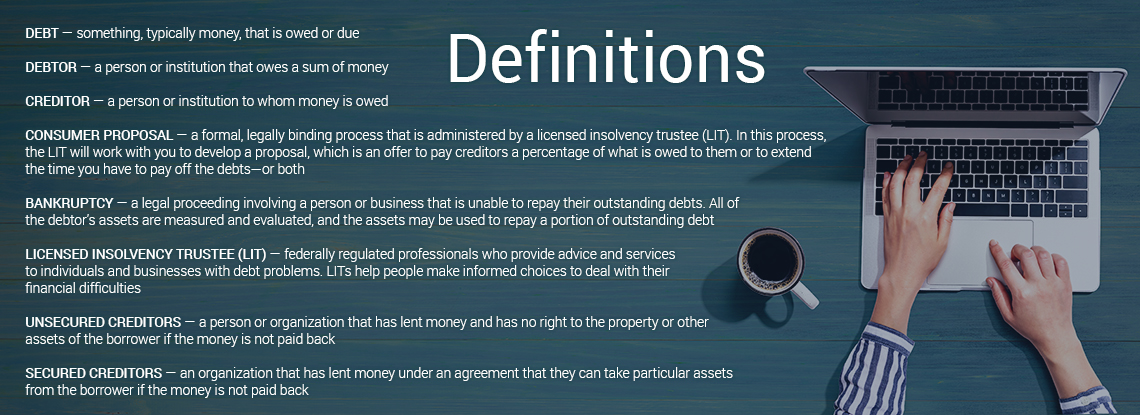

Definitions